(March 2026)

The UK Air Passenger Duty (APD) scheme is being reformed. The changes, taking place in 2026 and 2027, will result in drastic increases in the amount of duty paid by Business Jet Operators.

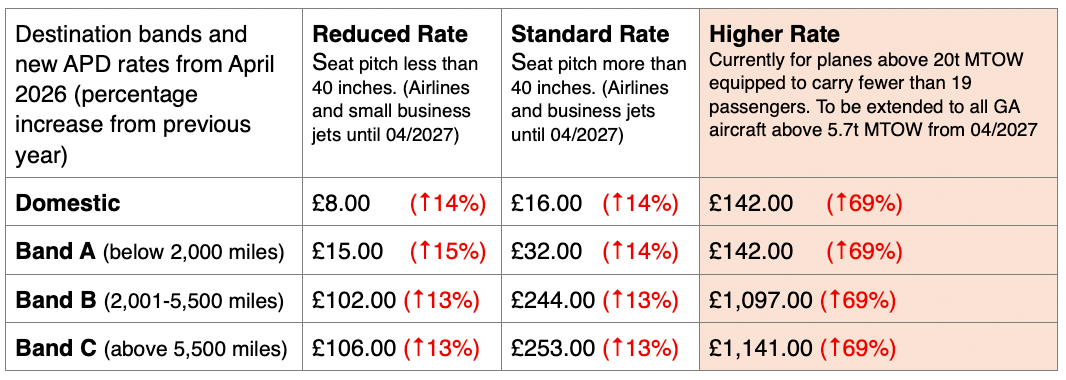

The first major increase in APD (69% for most heavy business jets) will go into effect in April 2026. More increases and changes to how APD is calculated for business aircraft are planned for April 2027.

As a reminder, the UK APD is a tax on flights departing from UK airports. It is charged per passenger carried on departure, and the amount to pay depends on the flight’s destination (band) and the class of travel (rate).

Destination (Band) – There are currently 4 destination bands:

- ‘Domestic’ for flights departing to destinations in England, Scotland, Wales, and Northern Ireland.

- Where the distance from London to the destination country’s capital is 0-2,000 miles

- Where the distance from London to the destination country’s capital is 2,001- 5,500 miles

- Where the distance from London to the destination country’s capital is over 5,500 miles

Class of Travel (Rate) – There are currently 3 Rates: Reduced, Standard, and Higher. Aircraft with a Maximum Take-off Weight (MTOW) of 20 tonnes or more -and- equipped to carry fewer than 19 passengers (most long-range business jets) pay the Higher Rate. However, since some newer business aircraft (such as Global 7000) are equipped with 19 seats or more, they are not covered by the Higher Rate. By applying the Standard Rate, these aircraft pay a significantly lower amount of APD than smaller business aircraft.

His Majesty’s Revenue and Customs (HMRC), the UK tax authority, aims to increase business aircraft taxation by revising the rate definitions to require all business aircraft (with MTOW above 5.7 tonnes / 12,566 lbs) to pay the Higher Rate from April 2027. Furthermore, HMRC has increased the Higher Rate by more than 100% in the last 4 years, and the increase in April 2026 represents a 69% jump from April 2025. UK APD is now the highest per-passenger aviation tax in the world.

Paying UK APD

Operators will still be required to report and pay their APD obligations through one of two schemes:

1. Occasional Operator Scheme (OOS) for Operators that meet the following criteria:

- Operate less than 12 flights from the UK in any 12 months

- Have an annual duty liability of less than £5,000

- Reporting through the OOS requires Operators to obtain a payment reference number from HMRC and report and pay their APD within 7 days of their flight.

2. Registered Operator Scheme – for Operators that do not meet the conditions to report through OOS.

- Reporting through the Registered Operator Scheme requires Operators to register their details with

- Non-UK Operators are also required to appoint a UK-based fiscal or an Administrative Representative to manage the account and to submit APD returns monthly, even when there is no flight activity from the UK.

Flight Pro International is registered as an Administrative Representative with HMRC and can calculate any APD due, file monthly returns, maintain all APD records, and pay on behalf of FPI clients.

Let’s have a conversation about how Flight Pro International can handle the legwork associated with the revised, incumbent UK APD. We’re here to ensure that your operations are as hassle-free as possible while moving throughout the UK region.

— — —

To learn more about FPI, FPC, or regarding the Compliance, Operations, Regulatory, and other Special Services Network (SSN) teams, please contact our Operations staff here at Flight Pro International.

Our success is your success! Partner with us today.